A Market Defined by Logistics Demand

The Inland Empire, Los Angeles County, and Orange County have quietly become the most consequential logistics hub in the United States. Sitting at the intersection of the world’s busiest port complex and a consumer base of 17.6 million people, this market is benefiting from e-commerce growth, supported by infrastructure that makes modern commerce function at scale.

Third-party logistics firms (3PLs) have emerged as the market’s dominant leasing force. Since the start of 2025, 3PLs have accounted for 48% of all leased square footage across the region in transactions of 50K+ SF, totaling 37.3 million square feet out of 78.3 million.

Larger Deals. Newer Buildings. Higher Specifications.

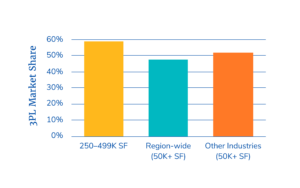

The data makes one thing unmistakably clear: 3PLs are leasing more space and doing so differently. The average 3PL lease stands at 213,208 square feet, a full 33% larger than the 160,476 square feet average across all other industries. In the 250,000–499,999 square feet size range, 3PLs account for 59% of all leased space.

What’s driving the size premium? Operational Complexity. Modern 3PLs require high clear heights to accommodate multi-level racking and automation systems, expansive truck courts for high-frequency carrier activity, and generous parking ratios for large labor pools. These requirements push 3PLs toward the newest, most purpose-built product in the market.

Nearly one quarter of all 3PL-leased space was in properties built since 2020, and 45% was in facilities developed since 2010. As automation investment continues to escalate across the industry, expect 3PLs to increasingly concentrate in Class A product and to create growing obsolescence risk in older industrial stock that cannot meet their technical requirements.

For owners and investors, this signals a durable, structurally driven premium for modern, high-spec industrial facilities. The buildings 3PLs want—and increasingly require—are not just preferred; they are the market.

A Dominant and Concentrated Force in The Inland Empire

Perhaps the most striking finding in recent leasing data is the significant activity of China-based 3PL operators. These firms represent 57% of all 3PL lease transactions of 50,000 square feet or larger across the Greater Los Leasing activity driven by 3PLs is reshaping the size, quality, and function of industrial demand. Angeles region (LA County, Inland Empire, and Orange County) and have leased 21.5 million square feet, or 36% more square footage than all other 3PL firms combined (15.8 million square feet), representing a commanding lead in total space absorbed.

Their geographic concentration is equally notable. Sixty-five percent of 3PL deals by China-based operators are occurring in the Inland Empire, where land availability, newer industrial supply, and proximity to the ports create an optimal operating environment. Drilling down further, 78% of these Inland Empire transactions are clustered in the West Inland Empire submarket.

China-based 3PL operators have shown a willingness to commit to long-term leases and large-block space, making them an important source of demand in the region. Changes in U.S.-China trade policy and global supply chain adjustments are factors to watch, but the scale of current leasing activity points to a sustained presence in the market.

Beyond the headline numbers, ground-level market activity reveals important nuance. China-based 3PL operators have been particularly active in sublease transactions, specifically facilities with existing racking and material handling equipment in place. These deals offer a compelling operational advantage: faster building access, accelerated startup timelines, and significantly reduced capital expenditure.

However, many of these operators are newly formed entities with limited operating history and thin f inancial profiles. In a market where vacant buildings can sit unabsorbed for 10 to 12 months, some landlords have executed leases with these higher-risk tenants, offset by above-standard lease securitization requirements. Over the past year, a notable number of these tenants have defaulted or vacated mid-lease, forcing landlords to recapture space and restart the marketing cycle ahead of natural lease expiration—a dynamic worth monitoring.

What Comes Next and Who Needs to Pay Attention

The structural forces underpinning 3PL demand in Greater Los Angeles are not cyclical. The region’s consumer density, port adjacency, and role as the primary gateway for trans-Pacific trade create a demand foundation that will outlast near-term economic fluctuations.

Landlords and Developers

The tenants driving this market have specific, non-negotiable physical requirements. Investing in clearheight upgrades, expanded truck courts, and power infrastructure capable of supporting automation is no longer speculative; it is a prerequisite for competitive positioning in this tenant pool.

Investors

The 3PL-driven demand story underpins what is arguably the most defensible industrial thesis in the Western U.S. Occupancy by sophisticated, logistics-native tenants in modern facilities near population and port density creates a compelling combination of income stability and long-term appreciation potential.

Occupiers

Competition for the right product is intensifying. The window to secure modern, well-located space at favorable terms narrows as 3PL demand continues to absorb new supply. Acting decisively, supported by the right market intelligence, is the key differentiator. Success in this market will favor stakeholders who anticipate the evolving needs of 3PL tenants. By aligning investments, leasing strategies, and property upgrades with these requirements, landlords, investors, and occupiers alike can position themselves to capture long-term value in a market increasingly defined by logistics-driven growth.