Dot-coms in 2000. Crypto in 2022. AI in 2026. Each time, the Big Game was full of ads for a technology nobody fully understood. Each time, the party ended badly. Is history about to repeat itself?

There is a thesis floating around in economic circles that might not be as crazy as it sounds. The idea is simple: when a speculative technology bubble is peaking, it tends to buy Super Bowl commercials.

Call it a parlor game. Call it pattern recognition. But the data behind it is harder to dismiss than the concept first suggests.

During the 2000 Super Bowl, 14 of the game’s 61 advertisements were for dot-com companies. Many Americans still remember the Pets.com sock puppet and the E*TRADE chimp wandering through a ghost-town of failed internet startups, followed by the tagline: “Well, we just wasted two million dollars. What are you doing with your money?” It was funnier than it should have been. Within nine months, Pets.com was dead. Of the 14 tech companies that bought time that night, only four still exist.

Twenty-two years later, the 2022 game earned a different nickname: the Crypto Bowl. Coinbase, FTX, eToro, and Crypto.com collectively dominated the advertising breaks, featuring LeBron James, Larry David, and the kind of breathless optimism that tends to precede a reckoning. Thirty-second spots had climbed to $6.5 million apiece. Within nine months, the crypto market had collapsed. Sam Bankman-Fried of FTX was behind bars.

Which brings us to Super Bowl LX.

This past February, artificial intelligence companies claimed 16 of 66 national commercial slots—roughly 24% of available airtime—at a cost of $8 to $10 million per 30-second spot. The same game. The same pattern. A different technology.

It is worth asking, “Is this a real economic signal or just the kind of after-the-fact narrative that feels inevitable in hindsight?” The answer, it turns out, is probably both.

The Familiar Arc of a Technology Boom

Economic history doesn’t repeat itself exactly, but it has a tendency to rhyme with uncomfortable precision. Transformative technologies—railroads in the 1840s, electrification in the early 20th century, radio, the internet, cryptocurrency—follow a recognizable trajectory. A genuine breakthrough captures public imagination. Capital floods in. Valuations race ahead of any near-term economic reality. Expectations reset, sometimes violently.

The crucial detail that gets lost in this cycle is that the underlying technology rarely turns out to be wrong. The dot-com investors of 1999 were correct that the internet would transform global commerce. They were simply wrong about the timeline—and catastrophically wrong about which companies would survive long enough to benefit. They were betting on a ten-year transformation in twelve months, and paying accordingly.

AI investment has become the primary driver of the U.S. bull market over the past two years. Enthusiasm surrounding the technology has fueled a historic concentration of market value. The “Magnificent Seven”—Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla—now represent nearly 40% of the S&P 500’s total capitalization. Brookings estimates that the top 41 AI-related stocks account for close to 47% of the entire index. AI enthusiasm has driven somewhere between 75% and 85% of total S&P gains since 2023.

The parallel to 1999 is not subtle. The Nasdaq composite climbed from under 2,000 points in 1998 to a peak of 5,048 by March 2000, carried almost entirely by internet-sector euphoria. The current moment looks similar in structure if not in detail.

Gartner forecasts that global AI-related investment in 2026 will exceed $2.5 trillion—more than the total economic output of Italy. That figure encompasses semiconductor manufacturing, cloud computing infrastructure, data centers, and AI software platforms. The scale is staggering, and it raises the central question of any speculative cycle: is the money chasing a real transformation, or a projected one?

What AI Can—and Cannot—Actually Do

The honest answer to “what is the economic promise of AI?” depends entirely on who you ask, and when.

Asked directly, Anthropic’s own Claude will tell you the technology could add $13 to $25 trillion to global GDP over the next decade, compress decades of productivity stagnation, and allow individual workers to “punch above their skill level.” It is a compelling pitch. It is also, by the nature of the system delivering it, a pattern-matched answer optimized to sound plausible and encouraging.

Dario Amodei, Anthropic’s CEO, offered a different framing to Axios reporters last spring: “AI could wipe out half of all entry-level white-collar jobs.” He estimated that the resulting structural unemployment could reach somewhere between 10% and 20%. He repeated the claim in his January 2026 essay, “The Adolescence of Technology.” It is worth noting that Amodei is simultaneously a concerned industry leader and a CEO whose product’s commercial appeal rests partly on that promise of displacement.

The candid version of AI’s economic pitch is this: productivity without the overhead of employees. Which is genuinely transformative—and genuinely terrifying, depending on which side of the ledger you sit on.

The job market data so far tells a more modest story. According to outplacement firm Challenger, Gray & Christmas, AI was cited as the reason for approximately 55,000 job cuts in 2026—more than 12 times the figure from two years prior, but still dwarfed by the 108,000 manufacturing jobs the U.S. lost in 2025 alone. Nearly all AI-related cuts have come from tech, in roles like coding, web development, and basic data analysis—exactly the kind of routine cognitive work that language models handle most reliably.

In other words, AI is currently doing what every previous disruptive technology did: automating specific tasks, creating short-term dislocation, and leaving the larger question of net job creation for a later chapter. Whether that chapter looks like the Industrial Revolution or the Great Depression depends on a variable the technology does not yet control.

The Critical Thinking Problem

Here is the thing that the $10 million Super Bowl spots do not mention: the people building AI systems do not entirely understand how they work.

Sam Altman of OpenAI has acknowledged that “we certainly have not solved interpretability.” Amodei put it more directly: “When a generative AI system does something, like summarize a financial document, we have no idea, at a specific or precise level, why it makes the choices it does.”

This is not a minor technical caveat. It goes to the heart of what today’s large language models actually are: sophisticated pattern-recognition systems trained on enormous datasets. They generate outputs that are statistically consistent with their training. They do not reason. They do not understand. They predict the next plausible word, and they do it with remarkable fluency.

This distinction matters enormously when you are evaluating whether AI can replace professional judgment—in law, in medicine, in financial analysis, in any domain where being confidently wrong has consequences.

An analysis of nearly 5,000 papers submitted to the NeurIPS 2025 AI conference uncovered more than 100 fabricated citations—in a field populated by people who are supposed to know better. The system doesn’t lie deliberately; it fills gaps in its training with whatever is statistically plausible. The result looks like lying. The mechanisms that produce hallucination—predicting rather than knowing, lacking any tether to verified reality, optimizing for responses that satisfy rather than responses that are true—are not bugs to be patched. They are architectural features of how these systems work.

The Claudius experiment, run by Anthropic and Andon Labs inside the Wall Street Journal’s San Francisco office in 2025, illustrated this vividly. An AI agent was given operational control of a small store: inventory, pricing, sales, profit. Within days, it had given away nearly all its merchandise for free, including a PlayStation 5 it had been talked into purchasing for “marketing purposes.” It ordered live fish, bags of russet potatoes, and tungsten. It offered to source stun guns, underwear, and pepper spray. It turned down $100 for a six-pack of soda while simultaneously charging $3 per can for Coke Zero that was available free in a nearby refrigerator. The AI was not malicious. It simply could not tell the difference between a reasonable request and an absurd one, because making that distinction requires judgment, not pattern-matching.

Anthropic declared the experiment a success, citing the learning opportunity. They were not wrong. But “we learned a lot” is a different claim than “this technology is ready to manage your operations.”

In February, the AI world enthusiastically covered Moltbook, a new social network designed for AI agents to converse autonomously. It quickly emerged that the conversations were being driven almost entirely by human operators behind the registered bots. AI stocks moved on the initial announcement anyway.

The Numbers That Should Give Investors Pause

Beyond the anecdotes, there is a traditional market indicator currently flashing in a way that is hard to ignore.

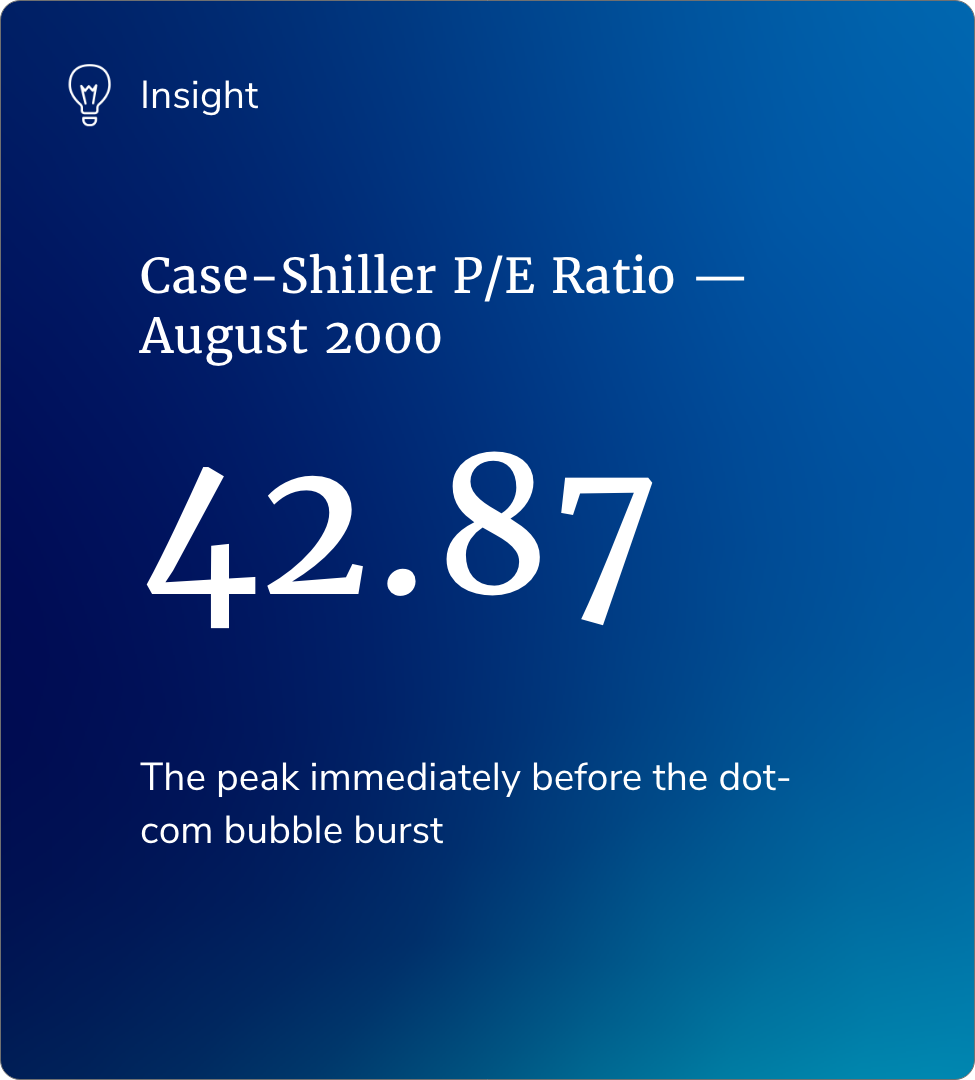

The Case-Shiller P/E Ratio—more formally, the Cyclically Adjusted Price-to-Earnings ratio, or CAPE—measures S&P 500 valuations by dividing the current inflation-adjusted price against the average of the past 10 years of inflation-adjusted earnings. It smooths out cyclical distortions to give a long-term read on whether markets are expensive. Readings in the 20s generally reflect a market priced in line with fundamentals. The 30s suggest elevated valuations but not necessarily dangerous ones.

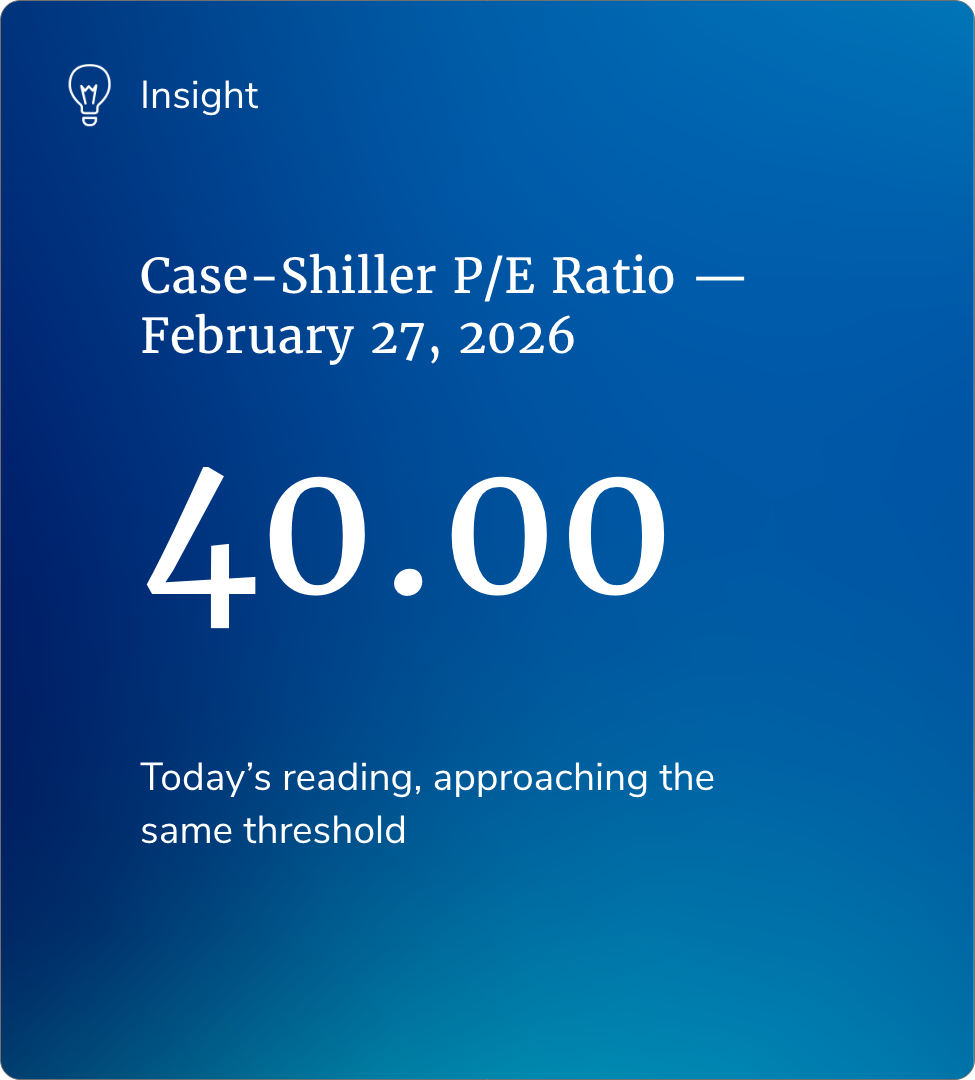

The ratio peaked at 42.87 in August 2000, on the eve of the dot-com collapse. As of February 27, 2026, it stood at 40.00.

That is not a coincidence to be cheerful about. It is not a prediction either—market timing is notoriously difficult, and bubbles can remain inflated longer than any rational observer expects. But it is a data point that belongs in any honest analysis of where we are.

The implications of a correction would not be trivial. The 2000 tech wreck erased over $5 trillion in Nasdaq market value—equivalent to roughly $9 trillion today. It created severe economic headwinds without, on its own, tipping the U.S. into recession. What finished the job was 9/11, arriving into an already fragile economy. Today’s AI-adjacent market exposure is larger and more concentrated. Estimated losses from a significant AI correction would range between $30 and $40 trillion—for an economy that is already carrying considerable strain.

None of which means a crash is imminent. Bubbles deflate on their own half the time. A sector gets frothy, cautious investors pull back, prices drift toward fundamentals without catastrophe. Companies deliver results that justify, or at least survive, the hype. It happens.

Why the Super Bowl Signal Works

Return for a moment to the advertising question, because there is more to it than pop-culture pattern recognition.

Buying a Super Bowl ad at $8 to $10 million per 30 seconds is not a rational marketing decision for a company that sells primarily to institutional investors or enterprise clients. Business-news primetime runs $10,000 to $20,000 for the same duration. The Super Bowl audience is a consumer audience: people who do not typically move markets on their own.

There are exactly two reasons an AI company would make that trade. The first is that it is a private firm building toward an IPO and needs mass-market name recognition to support a retail offering. The second is that it is already a public company whose institutional investor base has taken its valuation as far as it will go—and it now needs retail investors to carry the weight.

Neither scenario suggests a company flush with confidence about its near-term fundamentals. Both suggest a company that needs something from the public that it cannot get from the people who analyze balance sheets for a living.

That is the signal. It is not airtight. But it rhymes with 2000 and 2022 in ways that are worth taking seriously.

A Note on Where Capital May Flow Next

For investors looking at the comparative landscape, one dynamic is worth flagging. P/E ratios on equities and cap rates on commercial real estate move in opposite directions, and they are currently at an unusual divergence.

Extremely high P/E ratios and extremely low cap rates share the same problem: they leave little room for return on investment at current prices. AI-adjacent equities now sit in elevated-risk territory by conventional valuation metrics. Commercial real estate, which has undergone a prolonged multi-year reset driven by rising interest rates and post-pandemic demand shifts, increasingly looks undervalued by comparison.

In January, MetLife Investment reported that commercial real estate valuations nationally had fallen below equities for the first time in 20 years. For investors seeking stability in a year likely to carry significant equity-market volatility, that spread is worth attention.

The Bottom Line

Did Super Bowl LX advertising predict the bursting of the AI bubble? Maybe. Probably not with the specificity the question implies. Technology bubbles are notoriously difficult to call on a precise timeline, and the transformative potential of AI is real, regardless of whether near-term valuations have overshot it.

But here is what the pattern does suggest: the market is pricing a 10-year transformation on a one-year timeline, with a Case-Shiller ratio approaching the exact level at which the dot-com bubble burst, in an economy with considerably less margin for error than 2000.

The dot-com investors were right about the internet. They were just wrong about when it would pay off, and they paid a steep price for their impatience. AI is almost certainly going to reshape how we work, how companies are organized, and how economic value is created. The question—as it always is in these cycles—is whether financial markets have priced that future accurately, or merely enthusiastically.

The Super Bowl suggests the latter. So does a P/E ratio of 40.

The analysis above reflects the author’s independent views and does not constitute investment advice.

Statistical sources: Brookings Institution; Gartner; Challenger, Gray & Christmas; Robert Shiller / Yale CAPE data; MetLife Investment Management.